Killexams CEMAP-1 Exam Braindumps includes latest syllabus of Certificate in Mortgage Advice and Practice (CeMAP 1 UK) 2024 exam with up-to-date exam contents | Actual Questions - Mahfia.tv

PDF Exam Questions and Answers : CEMAP-1 Exam Braindumps contains complete pool of CEMAP-1 Questions and answers in PDF format. PDF contains actual Questions with May 2024 updated Certificate in Mortgage Advice and Practice (CeMAP 1 UK) 2024 Braindumps that will help you get high marks in the actual test. You can open PDF file on any operating system like Windows, MacOS, Linux etc or any device like computer, android phone, ipad, iphone or any other hand held device etc. You can print and make your own book to read anywhere you travel or stay. PDF is suitable for high quality printing and reading offline.

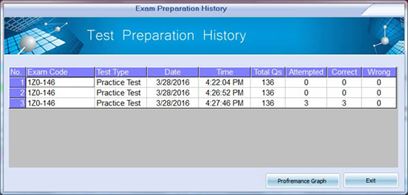

VCE Exam Simulator 3.0.9 : Free CEMAP-1 Exam Simulator is full screen windows app that is like the exam screen you experience in actual test center. This sofware provide you test environment where you can answer the questions, take test, review your false answers, monitor your performance in the test. VCE exam simulator uses Actual Exam Questions and Answers to take your test and mark your performance accordingly. When you start getting 100% marks in the exam simulator, it means, you are ready to take real test in test center. Our VCE Exam Simulator is updated regularly. Latest update is for May 2024.

Financial CEMAP-1 Exam Braindumps

We offer Financial CEMAP-1 Exam Braindumps containing actual CEMAP-1 exam questions and answers. These Exam Braindumps are very useful in passing the CEMAP-1 exams with high marks. It is money back guarantee by killexams.com

Real Financial CEMAP-1 Exam Questions and Answers

These CEMAP-1 questions and answers are in PDF files, are taken from the actual CEMAP-1 question pool that candidate face in actual test. These real Financial CEMAP-1 exam QAs are exact copy of the CEMAP-1 questions and answers you face in the exam.

Financial CEMAP-1 Practice Tests

CEMAP-1 Practice Test uses the same questions and answers that are provided in the actual CEMAP-1 exam pool so that candidate can be prepared for real test environment. These CEMAP-1 practice tests are very helpful in practicing the CEMAP-1 exam.

Financial CEMAP-1 Exam Braindumps update

CEMAP-1 Exam Braindumps are updated on regular basis to reflect the latest changes in the CEMAP-1 exam. Whenever any change is made in actual CEMAP-1 test, we provide the changes in our CEMAP-1 Exam Braindumps.

Complete Financial CEMAP-1 Exam Collection

Here you can find complete Financial exam collection where Exam Braindumps are updated on regular basis to reflect the latest changes in the CEMAP-1 exam. All the sets of CEMAP-1 Exam Braindumps are completely verified and up to date.

Certificate in Mortgage Advice and Practice (CeMAP 1 UK) 2024 Exam Braindumps

Killexams.com CEMAP-1 Exam Braindumps contain complete question pool, updated in May 2024 including VCE exam simulator that will help you get high marks in the exam. All these CEMAP-1 exam questions are verified by killexams certified professionals and backed by 100% money back guarantee.

Exam Code: CEMAP-1 Practice test 2023 by Killexams.com team CEMAP-1 Certificate in Mortgage Advice and Practice (CeMAP) The purpose and structure of the UK financial services industry

The Financial Conduct Authoritys (FCAs) main aims, activities and relevant Conduct of Business rules

The house-buying process and parties involved

The different types of customers and mortgages

How to assess the affordability and suitability of different mortgage options and associated products

Purpose and structure of the UK financial services industry.

• Financial Conduct Authority (FCAs) main aims, activities and relevant Conduct of Business rules.

• The house-buying process and parties involved.

• The different types of customer and their need for different types of mortgage.

• Assessment of affordability and suitability of different mortgage options and associated products.

- understand the structure and regulation of the UK financial services industry, asset classes and the interaction between the types of financial services products and clients requirements

- understand the main asset classes and features of financial services products, and the main financial advice areas

- understand the process of giving financial advice, the basic legal concepts, and the basic UK tax and benefits system

- understand the impact of inflation, interest rate volatility and other socio-economic factors relating to personal financial plans

- Detail Assess area

- understand the role of oversight groups, the requirements of the regulator and other laws relating to the provision of advice

- understand the non-tax laws, regulations and codes of conduct features of the regulators Conduct of Business Rules and how they apply to clients

- understand the regulator approach to regulation and how the rules affect the control and structures of firms

- understand how anti-money laundering regulations apply 7

- understand the main features of rules for dealing with complaints and how the Data Protection Act affects the provision of financial advice

- Detail Assess area

- know the regulatory definition of different types of mortgages, Buy to Let mortgages, Consumer Buy to Let mortgages, second charges and equity release

- know the house-buying process, the key parties involved and their roles 2

- know the process and implications of buying property at auction 3

- know the common types of borrower and how their main mortgage related requirements may differ and what factors may disqualify people from borrowing

- understand the main requirements of the Mortgage Conduct of Business Rules and the legislation affecting mortgages

- understand the economic and regulatory context for giving mortgage advice 6 Unit 4

Detail Assess area

- understand the role of a Mortgage Adviser 1

- understand the purpose of additional security, including the role of guarantors 2

- understand the fees and charges involved in arranging a mortgage 3

- know the principal types of property defect that surveys can identify and understand their implications when seeking a mortgage

- understand the principal factors affecting the value of property 5

- understand the different forms of valuation and survey 6

- understand the need to obtain Local Authority planning consent for house development/extensions

Detail Assess area

- understand the key features of the different types of mortgage repayment options and their benefits and drawbacks for different types of borrower

- understand the key features of the different types of mortgage product and interest rate options

- understand the main features and functions of different forms of life assurance and other insurances

Detail Assess area

- understand the principles and procedures associated with raising additional money and the circumstances when further borrowing might be appropriate

- understand the principles, procedures and costs of transferring mortgages 2

- understand the principles of using mortgages within debt consolidation arrangements 3

- understand the implications for the borrower of the non-payment of mortgages, other breaches of the Mortgage Deed, non-payment of building insurance and the options available

- understand the legal rights and remedies available to lenders in respect of non-payment from borrowers

- understand the main provisions made by the State to assist consumers in difficulties over the repayment of mortgages

Detail Assess area

- analyse consumers circumstances and suitable mortgage solutions taking account of any existing arrangements

- apply suitable mortgage solutions to specific consumers circumstances 2 Certificate in Mortgage Advice and Practice (CeMAP) Financial Certificate test Killexams : Financial Certificate test - BingNews

https://killexams.com/pass4sure/exam-detail/CEMAP-1

Search resultsKillexams : Financial Certificate test - BingNews

https://killexams.com/pass4sure/exam-detail/CEMAP-1

https://killexams.com/exam_list/FinancialKillexams : 8 Big Advisory Firms With Lots of CFPs

Slideshow August 21, 2023 at 12:13 PM Share & Print

A growing number of firms across the U.S. wealth management industry see hiring and developing talent with the certified financial planner (CFP) designation as an important part of their competitive strategy, especially as their clients demand deeper and more personalized planning experiences.

The approach makes a lot of sense, experts agree, as many in the public and in the industry view the CFP mark as one of the most important credentials a professional can attain when it comes to proving and maintaining their knowledge of the most important financial planning skills.

Advisors say that studying for the test and obtaining the CFP designation is a great way to obtain comprehensive planning knowledge that can then be applied toward building a practice or serving clients, depending on which area of the financial services profession one operates in.

In this sense, the focus on getting more CFPs in the door should come as no surprise, nor should the expanding efforts of firms to encourage their staffers to pursue the designation.

In fact, in the view of Penny Pennington, managing partner at Edward Jones, getting more CFP talent into the firm’s many branches is an essential strategy for the future, so much so that the firm has declared the goal of becoming the advisory organization with the most CFPs under one brand in the United States.

“We managed to get 600 CFPs through the program last year,” Pennington recently told ThinkAdvisor. “We have more than that are registered this year, and our goal is to have more than 4,000 CFPs on board by the end of the year.”

Pennington says she is particularly proud of the racial and gender diversity of the firm’s CFP talent, and she counts herself among the group of industry leaders who see the CFP Board’s efforts to improve the diversity of certificants as a critical initiative for the advisor industry as a whole.

“We all know from the pace of demographic change in our country that the next two generations of investors are going to be so much more diverse, and the advisory industry must change to reflect that,” Pennington says.

See the slideshow for information about eight firms that responded to an informal survey from ThinkAdvisor with information about their CFP representation. Rather than providing an apples-to-apples comparison, the list instead demonstrates the broad and deepening interest in the CFP designation among leading advisory shops.

Mon, 21 Aug 2023 04:13:00 -0500entext/htmlhttps://www.thinkadvisor.com/2023/08/21/8-big-advisory-firms-with-lots-of-cfps/Killexams : 7 easy & lucrative ways to earn money onlineNo result found, try new keyword!Most of us want to make extra money so that we can pay those bills that have been hanging over us like a sword or to run our house in a more smooth manner, or to cater to our shopping habits too.Wed, 23 Aug 2023 03:30:00 -0500en-ustext/htmlhttps://www.msn.com/Killexams : CHF 10 MILLION IN FINANCIAL SUPPORT FOR SIKA’S INNOVATIVE CONCRETE RECYCLING TECHNOLOGY

Sika AG

CHF 10 MILLION IN FINANCIAL SUPPORT FOR SIKA’S INNOVATIVE CONCRETE RECYCLING TECHNOLOGY

Sika’s innovative reCO2ver® technology is now receiving targeted support as part of a climate protection program. The technology involves a novel concrete recycling process that allows old concrete to be entirely reused while facilitating the sequestration of CO2. To support the use of the technology, Switzerland’s Climate Cent Foundation is guaranteeing the purchase of CO2certificates from the program for an initial amount of CHF 10 million.

Almost 40% of global CO2 emissions are attributable to the construction and building sector. Around 30 billion tons of concrete are produced each year, with demand continuing to increase. Although cement as a binding agent and concrete as a composite are important construction materials, producing them has an impact on climate change. According to estimates, the cement industry alone is responsible for more than 8% of global greenhouse gas emissions. With reCO2ver®, Sika has developed an innovative technology that is unique in the concrete sector and makes it possible to completely recycle concrete demolition waste. reCO2ver® is one of Sika’s many research and development activities focused on advancing the transformation of the construction industry toward greater sustainability.

17,000 TONS OF CO2SEQUESTRATION IN WASTE CONCRETE BY END 2030 Sika’s reCO2ver® technology not only separates old concrete into the high-quality individual components of gravel, sand, and cement stone; it can also bind additional CO2 through a chemical process. Around 15 kilograms of CO2 per tons of concrete demolition waste can be stored over the long term. On top of this, the performance of the cement stone powder produced during this process is optimized using Sika additives. This allows it to be repurposed as a substitute for cement in concrete production. A pilot facility has been operating in Switzerland since October 2021, and the test phase has now been completed successfully.

In order to be able to document the climate-added-value benefits of the reCO2ver® facilities on a standardized basis, Sika is working with South Pole on the development of a climate protection program aligned with the requirements of the Federal Office for the Environment (FOEN). A significant milestone in the implementation and use of this technology for CO2 capture and storage has now been achieved: Switzerland’s Climate Cent Foundation is guaranteeing the purchase of CO2 certificates from the program for an initial amount of CHF 10 million by the end of 2030.

The implementation of the industrial facilities is a central pillar of the certified climate protection program. By the end of 2030, the aim is to have stored approximately 17,000 tons of CO2 in concrete demolition waste. This is roughly equivalent to the amount of CO2 emissions produced during the construction of 850 concrete single-family homes.

Philippe Jost, Head Construction Sika: “Thanks to our innovative strength and sustainable technologies, we enable our customers in the construction and automotive sectors to reduce their ecological footprint. This drives the transformation toward greater sustainability. We are delighted that the reCO2ver® technology is being recognized through targeted support, and we are convinced that we are delivering significant added value to the construction industry, the environment, and future generations.”

SIKA CORPORATE PROFILE Sika is a specialty chemicals company with a globally leading position in the development and production of systems and products for bonding, sealing, damping, reinforcing, and protecting in the building sector and motor vehicle industry. Sika has subsidiaries in 103 countries, manufactures in over 400 factories, and develops innovative technologies for customers around the world that facilitate the sustainable transformation of the construction and transportation industries. With more than 33,000 employees, the company generated annual sales of CHF 10.5 billion in 2022.

The media release can be downloaded from the following link: Media Release

Wed, 23 Aug 2023 17:05:00 -0500en-UStext/htmlhttps://finance.yahoo.com/news/chf-10-million-financial-support-050000882.htmlKillexams : As MOC Debate Heats Up, Cardiology Societies Weigh In

It's no secret that many physicians question the value of Maintenance of Certification (MOC) requirements and are concerned about the amount of time, effort, and money the process takes. Now, they and at least two cardiology societies are starting to speak up.

MOC is an initiative from the American Board of Internal Medicine (ABIM) that requires an initial certification that costs thousands of dollars and must be repeated every 10 years. Annual MOC requirements involve tests that cost $220 for the first certificate a physician holds and about $120 for each subsequent one.

On July 21, hematologist-oncologist Aaron Goodman, MD, an associate professor at the University of California, San Diego, posted a petition on behalf of ABIM diplomates. It calls on ABIM to eliminate the MOC requirement because it is "burdensome," "costly," and "complex and time-consuming."

As of August 22, the petition had garnered more than 18,000 signatures.

Goodman recently debated ABIM President and Chief Executive Officer Richard J. Baron, MD, in a Healthcare Unfilteredpodcast. Before the debate, host Chadi Nabhan, MD, MBA, tweeted that he could not find a single physician who would defend the MOC and recertification.

L to R: Aaron Goodman, MD; Richard Baron, MD; and Chadi Nabhan, MD, MBA, discuss MOC on the Healthcare Unfiltered podcast.

The debate touched on Topics such as fees, evidence of value, the certification test format, and the cost and requirements to maintain more than one board certification. Overall, Goodman made the analogy to giving a patient chemotherapy: Because there are harms, he better know that there are also benefits. He cited that the harms associated with MOC include "financial toxicity, time toxicity, and stress toxicity," with the latter being particularly toxic to him personally.

Though the podcast gave both participants ample opportunities to express their views, it's not clear that either participant persuaded the other.

Cardiologists who are unhappy with MOC are speaking up on X (formerly Twitter). IC Matthew Sample, MD, listed five things he's done to Improve his practice since IC graduation, for which he received no MOC points.

In response, internist Artem Minalyan, MD, asked, "Hypothetically, if Dr Baron required an IC procedure, I wonder if he would request you to get all your MOC points prior to consenting."

SCAI and HRS Weigh In

Some professional societies have responded to the ABIM's threat to revoke the certifications of cardiologists who don't participate in periodic MOC activities.

The Society for Cardiovascular Angiography & Interventions (SCAI) published its "Position on ABIM Revocation of Certification for Not Participating in MOC." In it, SCAI states that ABIM diplomates who pass their exams and report procedural volumes as required should be "indisputably" recognized as "certified" for the relevant time frame (eg, 10 years), regardless of whether they participate in any other MOC activities.

SCAI President George D. Dangas, MD, PhD, told theheart.org | Medscape Cardiology that "Many of our members have expressed their frustration surrounding the confusion regarding their MOC requirements, including myself. We felt that this confusion could endanger the certified status of members, which would inevitably impact patient care, which is our greatest concern."

George D. Dangas, MD, PhD

The society has received an "overwhelmingly positive response" to its statement, he said. "Our hope is that ABIM will consider simpler, transparent regulations that are reflective of the feedback received from their constituents."

In response to the COVID-19 pandemic, ABIM extended the deadline for diplomates whose certificate expired in 2020 or 2021 until the end of 2022; Dangas suggests that ABIM further extend the deadline to enroll in or renew your MOC to the end of 2024 and that ABIM should "develop a recertification program that can be explained in a single slide/page."

The ABIM touts the value of MOC on its website, stating: "There is compelling evidence showing that MOC improves value of care without sacrificing quality and that board certified physicians command higher salaries."

Alternative options that are arguably less arduous are available.

In collaboration with ABIM, the American College of Cardiology (ACC) launched the ABIM/ACC Collaborative Maintenance Pathway (CMP) in 2019 as an alternative MOC assessment option.

The CMP "focuses on one or a small group of Topics within cardiology each year, incorporating learning activities as well as a pre-/post-formative knowledge assessment," Janice Sibley, ACC's executive vice president of Education and Publishing told theheart.org | Medscape Cardiology. The program continues to evolve, she said.

In 2022, she noted that the ACC increased the flexibility of the CMP by removing the 7-hour learning engagement requirement, allowing users to choose how much time to spend learning in the CMP program. They also extended the performance assessment windows from 7 to 9 days each, covering 2 weekends for each.

She said that to date, more than "6400 learners" are enrolled in the CMP program.

Though the collaboration seems to make MOC less onerous, some cardiologists think it makes the ACC "complicit."

A certification program that is independent of the ABIM launched in 2015. The National Board of Physicians and Surgeons (NBPAS) is a nonprofit organization led by an advisory board of unpaid physicians (including Medscape's editor-in-chief, Eric Topol, MD). NBPAS seems to be gaining momentum and acceptance.

Cardiologist Melissa Walton-Shirley, MD, recounted her recertification experience with the NBPAS late last year. She now maintains a "hybrid" certification with both ABIM and NBPAS. Though she wants to support the latter, she found that the alternative certification option still requires an initial ABIM certification and is not recognized in all states or by many insurers and hospitals.

Will MOC ever disappear? Sibley said that the ACC is always looking to Improve and enhance their offerings. "It is time to lead a change in the conversation from certification to continuous competency, from punitive to supportive options, from random knowledge testing to focused assessing knowledge gaps and lifelong learning. This will require innovation, technology, and new ways of thinking that offer cardiologists flexibility, relevance, and value and ultimately benefit the patients they serve."

Many physicians, including cardiologists, are hoping that the Goodman petition and further pressure from professional societies may finally translate into action.

Medscape LLC provides educational content including MOC. Medscape's editorial content, including news, features is developed independently of the educational content available on Medscape.

For more from the heart.org | Medscape Cardiology, follow us onTwitterandFacebook

Tue, 22 Aug 2023 08:55:00 -0500entext/htmlhttps://www.medscape.com/viewarticle/moc-debate-heated-cardiology-societies-weigh-2023a1000jjuKillexams : Congressman French Hill Sees Urgency In Congress To Pass Crypto LegislationNo result found, try new keyword!An exodus of American crypto companies offshore is creating momentum to finally pass needed legislation in congress.Wed, 23 Aug 2023 04:24:58 -0500en-ustext/htmlhttps://www.msn.com/Killexams : How to protect your financial life from wildfires, extreme weather

Comment

Watching the horrific wildfires in Maui and the people running for their lives might have you wondering what you would do if your home were in imminent danger.

Could you quickly put your hands on important financial documents while fleeing to safety?

“When we were evacuating, it felt almost like a video game,” said a 15-year-old Maui resident who, along with family, had to elude a wildfire. “We were like: ‘Pack your bags. … Take your valuables. You might lose your home.’”

Climate change has put many people in the path of major natural disasters. Fires, floods, hurricanes and wind storms are devastating communities.

As of Tuesday, there had been 15 confirmed weather/climate disaster events in the United States this year with losses exceeding $1 billion each, according to the National Centers for Environmental Information. Damage from 2022 disasters totaled $165.1 billion.

Swift-moving wildfires, fanned by winds from Hurricane Dora, have killed dozens in Maui. Video and photos show burned homes and businesses. Lahaina, a popular tourist destination in western Maui, was hard hit.

Right now, displaced residents are focusing on their basic needs — shelter and food.

However, many may soon face a new challenge — recovering pay stubs, insurance papers, bank statements and any of the other financial records that are the bane of our modern-day existence. Many businesses have been destroyed, raising the possibility of lost work records, too.

The disaster in Hawaii is just the latest reminder to get our financial houses in order. Here’s what you should do.

Prepare for a quick evacuation

Get a safe that’s waterproof, fire-resistant and light enough to carry. Keep all your household’s important financial documents in this box, including your passport; insurance policies; extra checks; a copy of your driver’s license; your Social Security card (or at least write down the number); bank, investment and credit card account numbers; and key legal documents such as wills, marriage and birth certificates, and the titles to your home and vehicles.

You should include some cash or traveler’s checks. If the electricity goes out, as it has in many areas in Maui, ATMs may not work and you might not be able to use a credit or debit card to make purchases.

Keep the original receipts of major purchases in the safe, as proof of what you spent.

Back up important financial documents

In addition to keeping your paperwork in a safe, make photocopies of your documents and place them in a safe-deposit box or deliver them to a trusted relative or friend who does not live in the same area you do.

You can also back up your data to cloud-based services such as Google Drive or Apple’s iCloud. Be sure to consistently back up your data to the cloud.

Make a list of major household items

With your smartphone, take pictures of your big-screen televisions, computers, furniture, heirlooms, etc. You want proof of the expensive stuff you own.

You might also want to record a video of the items in your home. Record model and serial numbers. Then, of course, download it for safekeeping in the event you have to prove to an insurance company what items you lost in a disaster.

Assess your insurance needs

Part of your disaster plan should be determining whether you’re carrying the right amount of insurance.

Now is the time to evaluate whether you have enough coverage. Call your insurance agent. Will your policy replace the full value of your possessions?

Do you have life insurance?

Many people neglect to get disability insurance. If you were injured in a natural disaster, would you be able to live off your savings? Buy enough disability insurance to replace 60 to 70 percent of your income.

What if your home is flooded?

Homeowners and renters insurance do not typically cover flood damage; coverage must be purchased separately. Even if you’re not in a high-flood-risk area, you may still need supplemental coverage.

The National Flood Insurance Program, managed by the Federal Emergency Management Agency, helps you purchase flood insurance from an insurance company or agent. If you need help finding a provider, go to floodsmart.gov/find or call 877-336-2627.

Just one inch of floodwater can cause up to $25,000 in damage, according to the NFIP.

On average, flooding causes more than $5 billion in damage nationwide each year, according to the NFIP. Hurricane Ian alone resulted in more than 46,000 claims and $1.5 billion in policy coverage.

You have to plan ahead, because typically there is a 30-day waiting period for an NFIP policy to go into effect, unless the coverage is mandated.

For information on flood insurance, go to floodsmart.gov.

Homeowners with mortgages have to carry homeowners insurance, but renters often neglect to protect themselves.

If you are renting, get renters insurance — the insurance your landlord carries does not cover damage to your personal possessions.

Natural disasters are only getting worse with climate change. It’s wise to be prepared in case your home or community is hit.

B.O.M. — The best of Michelle Singletary on personal finance

If you have a personal finance question for Washington Post columnist Michelle Singletary, please call 1-855-ASK-POST (1-855-275-7678).

Recession-proof your life: The tsunami of economic news is leading consumers, investors and would-be homeowners alike to ask whether a recession is inevitable. Regardless of the answer, there are practical steps you can take to help shield yourself from a worst-case scenario.

Money moves for life: For a more sweeping overview of Michelle’s timeless money advice, see Michelle Singletary’s Money Milestones. The interactive package offers guidance for every life stage, whether you’re just starting out in your career to living an abundant life in retirement.

Test Yourself: Do you know where you stand financially? Take our quiz and read advice from Michelle.

Thu, 10 Aug 2023 17:59:00 -0500Michelle Singletaryentext/htmlhttps://www.washingtonpost.com/business/2023/08/11/protect-financial-life-extreme-weather/Killexams : Ask the Financial Doctor: What is the earnings test for Social Security benefits?

Q: My neighbor donated some books and videos to the library. Can my neighbor take a deduction on the Michigan tax return?

A: There is no tax credit or deduction for donations to a library on the Michigan tax return.

Q: Is there a maximum age at which I will be forced to file for my Social Security benefits?

A: No, the Social Security Administration will not compel you to take your benefits. Taking benefits ahead of full retirement age (FRA) will result in a permanent reduction, postponing benefits past your FRA will increase your benefits by 8% per year up to age 70. Waiting beyond age 70 makes no sense because you could lose some monthly benefits. If you forget to file upon turning 70, you can apply for retroactive benefits up to six months.

Q: Can my Social Security check be garnished by a creditor?

A: Private creditors cannot garnish Social Security checks but the federal government can. If you defaulted on a VA or student loan or you owe money to the IRS or Medicare or are required to pay child support, then the federal government can garnish part of your Social Security check. The garnishment is usually 15% but could be as high as 60% for child support.

Q: What is the definition of the primary insurance amount (PIA) that the Social Security Administration calculates?

A: The primary insurance amount (PIA) is the Social Security benefit that you would receive at your full retirement age (FRA). Your benefits are reduced if you receive benefits earlier and are increased by 8% per year up to age 70 if you start benefits after your FRA.

Q: I am applying for a mortgage and need my tax returns for the last two years. How do I get them from the Internal Revenue Service?

A: Copies of your tax returns are generally available for the current tax year and as far back as six years. The fee per tax year is $43. Complete and mail form 4506 to request a copy of your tax return. Most lenders will accept a tax return transcript. A tax return transcript shows most line items and is free. You can request a transcript online, by phone or mail.

Q: Can I borrow money from my IRA?

A: No, there is no such thing as an IRA loan.

Q: If I lose Social Security benefits due to the earnings test, are they permanently lost?

A: No, the Social Security benefits are not permanently lost. The withheld amount will be restored as a delayed retirement credit, which will increase your Social Security benefits once you reach full retirement age (FRA).

Q: What is the earnings test for Social Security benefits?

A: The earnings test determines how much of your Social Security benefits are reduced when you have wages. The reduction depends on your age. If you are under full retirement age (FRA) for all of 2023, you would forfeit $1 in benefits for every $2 earned over $21,240. For example, if you applied for Social Security at 62 and earned $40,000 this year, you would lose $9,380 in benefits ($40,000 – $21,240 = $18,760 ; $18,760/2 = $9,380). There is no earnings test for wages after you reached FRA.

Q: When are estimated taxes due?

A: The year is divided into four payment periods, or due dates. Those dates generally are April 15, June 15, Sept. 15 and Jan. 15 (next tax year). Form 1040ES provides the instructions, worksheets, schedules and payment vouchers. The easiest way to pay estimated taxes is electronically through the Electronic Federal Tax Payment System or EFTPS. You can also pay estimated taxes by check or money order using the payment voucher that comes with form 1040ES.

Q: My uncle passed away two years ago and I believe there is an unclaimed insurance policy covering my uncle. How do I check for the missing insurance policy? If it exists how do I make a claim?

A: If you know the name of the insurance company contact them. If you do not know the name contact the large insurance companies, AIG, John Hancock, MetLife, Nationwide and Prudential. Several insurance companies have online tools for finding lost policies. Use the site, missingmoney.com, to search for missing insurance policies. After a lost policy is found, you need to provide a death certificate and proper beneficiary proof to claim the insurance.

Q: I have a ROTH IRA valued at $166,000. My total contributions were $77,000 with the balance being investment earnings. Can I take out the $77,000 anytime without penalty?

A: Yes, your contributions can be taken anytime without penalty. The investment earnings would incur a 10% penalty and be taxable if withdrawn before 59½ or if the account is under five years old. There are some exceptions to the 10% penalty such as payment for education, paying for a first-time home purchase and if you become disabled. If you’ve met the five-year holding requirement, and you are older than 59½ you can withdraw money from a Roth IRA with no taxes or penalties.

Helpful telephone numbers for any tax concerns:

• IRS Help (800) 829-1040 • MI Help (517) 636-4486

• IRS Forms (800) 829-3676 • MI Forms (517) 636-4486

Richard Rysiewski, a Certified Financial Planner, welcomes all questions on tax and financial matters. Please send to Richard Rysiewski, Financial Doctor, 3001 Hartford Lane, Shelby Twp., MI 48316.

Wed, 09 Aug 2023 23:18:00 -0500Richard Rysiewskien-UStext/htmlhttps://www.macombdaily.com/2023/08/10/ask-the-financial-doctor-what-is-the-earnings-test-for-social-security-benefits/Killexams : Tax Regs Address Overwithholding With Qualified Derivatives Dealers Exemption

Law, Rules, Standards, Agreement, Contract

getty

Section 871(m) treats payments under equity derivative contracts that reference U.S.-source dividends as if they are equivalent to U.S.-source dividends, potentially triggering a U.S. withholding tax.

Reg. section 1.871-15(q) interprets section 871(m) to exempt qualified derivatives dealers (QDDs) from tax and withholding requirements if overwithholding would occur. Published September 12, 2022, Notice 2022-37, 2022-37 IRB 234, delays the applicability date of some of the QDD provisions.

Dividend equivalents treated as U.S.-source dividend income are subject to a 30 percent U.S. tax when received by nonresident alien individuals and foreign corporations. The tax must be withheld by the dividend equivalent payer.

Final regs published in T.D. 9734 on September 18, 2015, generally became effective on that date. Those regs were revised and supplemented by final regs published January 24, 2017 (T.D. 9815), and December 17, 2019 (T.D. 9887).

The regs provide guidance to NRAs and foreign corporations holding financial products that provide for payments contingent upon, or determined by reference to, U.S.-source dividend payments. They also provide guidance to withholding agents responsible for withholding U.S. tax on dividend equivalent payments.

This article covers the guidance for QDDs in reg. section 1.871-15(q). Previous articles covered:

the delta calculation in paragraph (g) that determines whether a simple contract is a section 871(m) transaction (Tax Notes Int’l, July 3, 2023, p. 33);

the substantial equivalence test in paragraph (h) that determines whether a complex contract is a section 871(m) transaction (Tax Notes Int’l, July 10, 2023, p. 204);

the description of dividend equivalent payments and amounts in paragraphs (i) and (j) (Tax Notes Int’l, July 24, 2023, p. 415);

the definition of dividend equivalents (and exceptions) in subparagraphs (c)(1) and (2), and the antiabuse rule in paragraph (o) (Tax Notes Int’l, July 31, 2023, p. 557);

the exception to withholding in paragraph (l) for potential section 871(m) transactions that reference qualified indexes (Tax Notes Int’l, Aug. 7, 2023, p. 709); and

the requirements in paragraph (n) to combine transactions when testing whether they are subject to section 871(m) (Tax Notes Int’l, Aug. 14, 2023, p. 1066).

Section 871(m)nder section 871(a)(1), U.S.-source income of an NRA (other than capital gains) that is not connected with a U.S. business is subject to a 30 percent tax. This includes U.S.-source dividend income. Section 871(m)(1)-(7) addresses treatment under section 871(a) of dividend equivalents paid to an NRA. Reg. section 1.881-2(b)(3) directs taxpayers to section 871(m) and regs for rules applicable to dividend equivalents paid to foreign corporations.

The general rule in paragraph (m)(1) is that a dividend equivalent is treated as a U.S.-source dividend subject to the 30 percent tax. Paragraph (m)(2) generally defines a dividend equivalent as a payment contingent upon, or determined by reference to, a U.S.-source dividend. The descriptions in subparagraphs (m)(2)(A)-(C) are:

(A) any substitute dividend made under a securities lending or sale-repurchase transaction that is directly or indirectly contingent on, or determined by reference to, the payment of a dividend from U.S. sources;

(B) any payment made under a specified notional principal contract (NPC) that is directly or indirectly contingent on, or determined by reference to, the payment of a dividend from U.S. sources; and

(C) any other payment determined by the secretary to be substantially similar to a payment described in subparagraph (A) or (B).

The definition of specified NPC in paragraph (m)(3) is divided between payments made before and those made after the date that is two years after the March 18, 2010, enactment date of subsection (m) in the Hiring Incentives to Restore Employment Act.

Under the temporary definition in subparagraph (m)(3)(A) for payments made before March 18, 2012, a specified NPC has one of the following characteristics described in clauses (i)-(v):

(i) for entering into the contract, a long party transfers the underlying security to a short party;

(ii) for terminating the contract, a short party transfers the underlying security to a long party;

(iii) the underlying security is not readily tradable on an established securities market;

(iv) for entering into the contract, the underlying security is posted as collateral by a short party with a long party; or

(v) the contract is identified by the secretary as a specified NPC.

Under the definition in subparagraph (m)(3)(B) for payments made after March 18, 2012, all NPCs are specified NPCs unless the secretary determines that the contract does not have the potential for tax avoidance.

Subparagraph (m)(4)(A) defines long party as a party to the contract entitled to receive a payment that is contingent upon, or determined by reference to, the payment of a dividend from sources within the United States on the underlying security. Subparagraph (m)(4)(B) defines short party as a party to the contract that is not a long party.

Subparagraph (m)(4)(C) defines underlying security as the security requiring the dividend payment referred to in subparagraph (m)(2)(B). An index or fixed basket of securities is treated as a single security.

Under paragraph (m)(5), a payment includes a gross amount used in computing the net amount that is transferred to or from the taxpayer.

To prevent overwithholding on a chain of dividends or dividend equivalents, paragraph (m)(6) allows the secretary to reduce tax to the extent the taxpayer can establish that tax has been paid on another dividend equivalent in the chain, is not otherwise due, or is appropriate to address the role of financial intermediaries in the chain. This concern is addressed by the QDD provisions in reg. section 1.871-15(q)(1)-(5).

Paragraph (m)(7) describes coordination with withholding requirements under chapters 3 (sections 1441-1464) and 4 (sections 1471-1474). Each person that is a party to a contract or other arrangement that provides for the payment of a dividend equivalent is treated as having control of the payment.

The practical effect of section 871(m) is to change the source of a dividend equivalent payment from non-U.S. to U.S. The payment’s source is determined by the underlying U.S. security rather than the long party’s residence.

a general rule that treats dividend equivalents as U.S.-source dividends;

a definition of dividend equivalent, along with five exceptions;

a definition of specified NPC;

a definition of specified equity-linked instrument (ELI);

a description of substantially similar payments;

a calculation of delta (with two examples);

a test for substantial equivalence (with one example);

a description of dividend equivalent payments (with two examples);

the amount of a dividend equivalent;

a limit on treating corporate acquisitions as section 871(m) transactions;

treatment of derivatives that reference indexes;

treatment of derivatives held by partnerships;

treatment of combined transactions;

an antiabuse rule;

information reporting requirements (with one example);

a definition of QDD (with three examples); and

applicability dates.

Definitions

Subparagraphs (a)(1)-(15) provide definitions, some of which are particularly relevant to the application of the QDD rules in paragraph (q).

Subparagraph (a)(1) defines a broker by cross-reference to its meaning in section 6045(c), except that it does not include any corporation that is a broker solely because it regularly redeems its own shares.

Subparagraph (a)(4) defines an ELI as a financial transaction (other than a securities lending transaction, sale-repurchase transaction, or NPC) that references the fair market value of one or more underlying securities — for example, a futures contract, forward contract, option, debt instrument, or other contractual arrangement that references the FMV of one or more underlying securities.

Subparagraph (a)(5) defines an initial hedge as the number of underlying security shares that a short party would need to fully hedge an NPC or ELI (whether the NPC or ELI is a complex contract or simple a contract benchmark within the meaning of subparagraph (h)(2)) at the calculation time for the NPC or ELI, even if the short party does not, in fact, fully hedge the NPC or ELI.

Subparagraph (a)(7) defines an NPC by cross-reference to its meaning in reg. section 1.446-3(c).

Subparagraph (a)(9) provides a multifaceted definition of transaction parties. A long party is entitled to receive a dividend equivalent, and a short party is obligated to pay a dividend equivalent. A party includes a long or short party, an agent acting on behalf of a long or short party, and a transaction intermediary.

If a potential section 871(m) transaction references more than one underlying security, the long party and short party are determined separately for each underlying security. A person is both a long and a short party when it is:

entitled to receive a payment that references a dividend payment on an underlying security; and

obligated to make a payment that references a dividend payment on another underlying security.

Subparagraph (a)(12) defines a section 871(m) transaction as a securities lending transaction, sale-repurchase transaction, specified NPC, or specified ELI. A potential section 871(m) transaction is a securities lending or sale-repurchase transaction, NPC, or ELI that references one or more underlying securities.

Subparagraph (a)(14) distinguishes between simple and complex contracts. A simple contract is an NPC or ELI that, for each underlying security, allows all amounts to be paid or received on the maturity, exercise, or other payment date to be calculated by reference to a single, fixed number of shares.

This assumes that the number of shares can be ascertained at the calculation time of the contract and that there is a single maturity or exercise date for which all amounts (other than upfront or periodic payments) are required to be calculated for the underlying security. A complex contract is generally an NPC or ELI that is not a simple contract.

Subparagraph (a)(15) defines an underlying security as an interest in an entity if that interest could deliver rise to a U.S.-source dividend under reg. section 1.861-3. If a potential section 871(m) transaction references an interest in more than one entity or different interests in the same entity, each referenced interest is a separate underlying security.

General Rule

Paragraph (b) repeats the general rule in section 871(m)(1) that treats a dividend equivalent as a dividend from sources within the United States in applying:

section 871(a) (noneffectively connected income of NRAs);

section 4948(a) (taxation and denial of exemptions for some foreign organizations); and

chapters 3 and 4 (withholding on foreign persons and some foreign accounts).

Dividend Equivalents

Subparagraph (c)(1) describes payments that are dividend equivalents, and subparagraph (c)(2) provides exceptions.

Subdivisions (c)(1)(i)-(iv) define a dividend equivalent as a payment that:

references a dividend from an underlying security under a securities lending or sale-repurchase transaction;

references a dividend from an underlying security under a specified NPC described in paragraph (d);

references a dividend from an underlying security under a specified ELI described in paragraph (e); or

is any other substantially similar payment as described in paragraph (f).

Specified NPCs and ELIs

Specified NPCs. Paragraph (d) defines specified NPCs. Subparagraph (d)(1) generally repeats the conditions in the temporary definition in section 871(m)(3)(A) and applies them to payments made after March 18, 2012, and before January 1, 2017.

Subparagraph (d)(2) applies to specified NPCs entered into on or after January 1, 2017, and treats simple and complex NPCs differently.

Under subdivision (d)(2)(i), a simple NPC that has a delta of 0.8 or greater in an underlying security at the calculation time is a specified NPC. Under subdivision (d)(2)(ii), a complex NPC that meets the substantial equivalence test in paragraph (h) at the calculation time is a specified NPC.

Specified ELIs. Paragraph (e) defines specified ELIs. Under subparagraph (e)(1), a simple ELI that has a delta of 0.8 or greater at the calculation time is a specified ELI. Under subparagraph (e)(2), a complex ELI that meets the substantial equivalence test in paragraph (h) at the calculation time is a specified ELI.

Delta and Substantial Equivalence

The delta calculation applies to determine whether simple NPCs and ELIs are specified. The substantial equivalence test applies to make this determination for complex NPCs and ELIs.

Delta. The delta calculation covered in subparagraphs (g)(1)-(5) determines whether a simple contract is a specified contract and therefore a section 871(m) transaction. The delta reveals the extent to which a derivative instrument traces its underlying security’s value. The higher a derivative’s delta, the more economically equivalent it is and the more closely its FMV tracks that of the underlying security. A delta-one derivative tracks the underlying security on a dollar-for-dollar basis.

A derivative instrument with a delta of 0.8 means that for every $1 the underlying security’s FMV varies, the derivative instrument’s FMV varies by $0.80. Simple contracts with a delta of at least 0.8 (and complex contracts meeting the substantial equivalence test) are replicating the economic benefits of holding U.S. securities and are subject to section 871(m).

Delta is the ratio of change in the FMV of an NPC or ELI to a small change in the FMV of the number of shares of the underlying security (as determined under subparagraph (j)(3)):

delta = change in FMV of NPC or ELI/change in FMV of underlying security sharesSubstantial Equivalence. The substantial equivalence test covered in subparagraphs (h)(1)-(7) applies to determine whether a complex contract is a specified contract and therefore a section 871(m) transaction. The test assesses whether a complex contract substantially replicates the economic performance of the underlying security by comparing at various testing prices for the security:

the differences between the expected changes in the FMV of the complex contract and its initial hedge; and

the differences between the expected changes in the FMV of a simple contract benchmark (as described in subparagraph (h)(2)) and its initial hedge.

The complex contract is a section 871(m) contract if, when the substantial equivalence test is applied at the calculation time for the complex contract, the expected change in the FMV of the complex contract and its initial hedge is equal to or less than the expected change in the FMV of the simple contract benchmark and its initial hedge.

Exceptions to Dividend Equivalents

Subdivisions (c)(2)(i)-(v) provide exceptions to dividend equivalent status for:

dividend equivalents received by a long party on an instrument that gives rise to a dividend under section 305(b) or (c);

payments made under a due bill;

payments made under annuity, endowment, or life insurance contracts; and

payments made under employee compensation arrangements.

Paragraph (k) of the regs provides an exception for payments related to corporate acquisition transactions that, as part of a plan, obligate the long party to acquire underlying securities representing more than 50 percent of the issuer’s FMV.

Paragraph (l) provides that payments under contracts that reference qualified indexes are generally not subject to U.S. tax withholding under section 871(m). Qualified indexes are widely used passive indexes based on a diverse basket of publicly traded securities.

Combined Transactions

Paragraph (n) operates to combine potential section 871(m) transactions to determine whether they collectively meet the tests for being subject to section 871(m). The goal of these rules is to prevent taxpayers from splitting a section 871(m) transaction into component transactions to avoid dividend equivalent treatment.

QDDs

The QDD rules are intended to prevent multiple withholdings on the same dividend stream. For example, if a foreign corporation owns U.S. stock and enters into a short forward contract with another foreign corporation, it generally will be subject to withholding on dividends paid on the stock. It will also have to withhold on dividend equivalent payments under the forward contract. The withholding tax on the dividend equivalent payments is effectively a second withholding tax.

Foreign financial institutions and clearing houses can receive U.S.-source dividends and dividend equivalent payments without being subject to withholding tax if they certify to the withholding agent that they are receiving the payments as custodians and not beneficial owners and they have entered into a qualified intermediary agreement with the IRS under which they assume primary withholding responsibility.

However, absent the QDD rules, dealers cannot act as QIs if they received the payments as beneficial owners of a hedge to transactions in which they are short parties. The regs address potential overwithholding by expanding the QI regime in section 1441 regs to include QDDs.

Therefore, regs under sections 871 and 1441 govern dividends and dividend equivalents received by a QDD. This article covers the section 871 provisions.

Reg. section 1.871-15(q) addresses taxation of dividend and dividend equivalent payments made to a QDD.

The guidance in subparagraphs (q)(1)-(5) include:

a general description of a QDD’s tax liability on dividend equivalent payments;

a capacity presumption for transactions reflected in a QDD’s equity derivatives dealer book;

a definition of the “section 871(m) amount” for each dividend on each underlying security;

a description of the net delta exposure calculation; and

three examples.

Sections881and1441.Section 881 generally taxes income of foreign corporations that is not connected to a U.S. business. Section 881(a)(1) imposes a 30 percent tax on U.S.-sourced interest, dividends, rents, salaries, wages, premiums, annuities, compensations, remunerations, emoluments, and other fixed or determinable annual or periodical gains, profits, and income.

Section 1441 generally requires the payers of these types of income to deduct and withhold the 30 percent tax when the income recipient is an NRA. Section 1442 requires payers to comply with the section 1441 withholding requirements when the income recipient is a foreign corporation.

Reg. section 1.1441-1(e)(5) provides guidance on QIs and withholding certificates, agreements, and statements. Reg. section 1.1441-1(e)(6) provides guidance on QDDs and prescribes the circumstances in which a QI can act as a QDD.

Reg. section 1.1441-1(b)(4)(xxii) provides that a withholding agent making a payment to a QI acting as a QDD is not required to withhold on specific payments if the agent can associate the payment with a valid QI withholding certificate (as described in reg. section 1.1441(e)(3)(ii)). Withholding is not required on a payment:

made under a potential section 871(m) transaction that is not an underlying security;

of a dividend equivalent; or

of a dividend in 2017.

QDD Tax Liability. Under reg. section 1.871-15(q)(1), a QDD described in reg. section 1.1441-1(e)(6) that receives a dividend equivalent payment in its equity derivatives dealer capacity will not be liable for tax under section 881 on that payment, provided that the dealer complies with its obligations under the QI withholding agreement described in reg. section 1.1441-1(e)(5)-(6).

A QDD is liable for tax under section 881(a)(1) on its section 871(m) amount for each dividend on each underlying security. This tax liability is reduced (but not below zero) by the amount of tax paid by the QDD under section 881(a)(1) on dividends it receives on that underlying security on that same dividend in its capacity as an equity derivatives dealer.

Also, a QDD is liable for tax under section 881(a)(1) for all dividend equivalents not received in its equity derivatives dealer capacity. A QDD is also liable for tax under section 881(a)(1) for all dividends it receives, other than dividends received in 2017, in its equity derivatives dealer capacity.

Paragraph (q) does not apply to a QDD that is a foreign branch of a U.S. financial institution (within the meaning of reg. section 1.1471-5(e)).

Capacity Presumption. Under subparagraph (q)(2), in determining the QDD’s tax liability, transactions properly reflected in a QDD’s equity derivatives dealer book are presumed to be held by the dealer in its equity derivatives dealer capacity. To determine whether a dealer is acting in its equity derivatives dealer capacity, only the dealer’s activities as an equity derivatives dealer are taken into account.

A dividend or dividend equivalent is treated as received by a QDD not acting in its equity derivatives dealer capacity if received by a QDD acting as a proprietary trader.

Section 871(m)Amount. Under subparagraph (q)(3), for each dividend on each underlying security, the section 871(m) amount is the product of:

the QDD’s net delta exposure to the underlying security for the applicable dividend; and

the applicable dividend amount per share.

Net Delta Exposure. Under subdivisions (q)(4)(A)-(B), the net delta exposure to an underlying security is based on the aggregate number of shares of an underlying security to which the QDD has exposure because of positions in the security (including owning the security). The net delta exposure measured in the number of shares compares the long and short positions and equals:

the number of shares in the underlying security in which the QDD has positions with FMVs that move in the same direction as the security (the long positions); minus

the number of shares in which the QDD has positions with FMVs that move in the opposite direction from the security (the short positions).

The net delta exposure calculation only includes long positions and short positions that the QDD holds in its equity derivatives dealer capacity (as described in subparagraph (q)(2)). Any long positions or short positions that are treated as effectively connected with the QDD’s U.S. trade or business are excluded from the net delta exposure calculation.

The net delta exposure to an underlying security is determined at the end of the day on the date provided in subparagraph (j)(2) for the applicable dividend. This is the earlier of:

the record date of the dividend; and

the day before the ex-dividend date.

For example, if a specified NPC provides for a payment at settlement that takes into account an earlier dividend payment, the amount of the dividend equivalent is determined on the earlier of the record date or the day before the ex-dividend date for that dividend.

Net delta must be determined in a commercially reasonable manner. If a QDD calculates net delta for nontax business purposes, the net delta ordinarily will be the delta used for that purpose, subject to the modifications required by this definition.

Each QDD must determine its net delta exposure separately only taking into account transactions that are recognized and attributable to that QDD under U.S. tax law.

Examples. Subparagraph (q)(5) provides three examples that illustrate the rules of paragraph (q). Example 1 illustrates the results of a forward contract between a foreign equity derivatives dealer and a foreign customer that is hedged with a total return swap between the foreign dealer and a U.S. broker.

Foreign bank FB is a QI that acts as a QDD. On April 1, year 1, FB enters into a cash settled forward contract initiated by a foreign customer that:

entitles the customer to receive from FB all appreciation and dividends on 100 shares of stock X; and

obligates the customer to pay FB any depreciation on 100 shares of stock X at the end of three years.

FB hedges the forward contract by entering into a total return swap contract with a domestic broker that is maintained as a hedge for the duration of the forward contract. The swap contract:

entitles FB to receive an amount equal to all dividends on 100 shares of stock X;

obligates FB to pay an amount referenced to a floating interest rate each quarter; and

provides for FB to receive from or pay to the broker (as the case may be) the difference between:

the FMV of 100 shares of stock X at the inception of the swap; and

the FMV of 100 shares at the end of three years.

Stock X pays a quarterly dividend of $0.25 per share.

At the end of the day on the date provided in subparagraph (j)(2) for the dividend, FB owns the forward contract and the total return swap. FB does not own any shares of stock X or any other transactions that reference stock X.

FB provides valid documentation to the broker that FB will receive payments under the swap contract in its capacity as a QDD, and FB contemporaneously enters both the swap contract with the broker and the forward contract with the customer on its equity derivatives dealer books.

At the end of the day on the date provided in subparagraph (j)(2) for the dividend, FB is a long party on a delta-one contract (the total return swap with the broker) and also a short party on a delta-one contract (the forward contract with the customer). Under reg. section 1.1441-1(b)(4)(xxii), the broker is not obligated to withhold tax on the dividend equivalent payments to FB on the swap contract referenced to stock X dividends because the broker may rely upon valid documentation to treat the payment as made to FB acting as a QDD.

Under subparagraph (q)(1), FB is not liable for tax under sections 871(m) and 881 on the payments it receives from the broker referenced to stock X dividends because FB’s net delta exposure on the 100 shares of stock X is zero at the end of the day on the date provided in subparagraph (j)(2) for the dividend.

The net delta exposure is zero because the taxpayer has:

100 shares of stock X long position exposure because of the total return swap; minus

100 shares of stock X short position exposure because of the forward contract.

FB is required to withhold tax on dividend equivalent payments to the customer on the forward contract in accordance with reg. section 1.1441-2(e)(7).

Example 2 illustrates an at-the-money call option contract (meaning the contract price is close or equal to the spot price) entered into by a foreign equity derivatives dealer that is hedged with a total return swap. The facts are the same as in Example 1, but the customer purchases from FB an at-the-money call option on 100 shares of stock X with a term of one year. The call option has a delta of 0.5, and FB hedges the call option by entering into a total return swap that references 50 shares of stock X with the broker.

At the end of the day on the date provided in subparagraph (j)(2) for the dividend, the call option has a delta of 0.6, FB hedges the call option with a total return swap that references 60 shares of stock X with the broker, and FB has no shares of stock X or other transactions that reference stock X.

At the end of the day on the date provided in subparagraph (j)(2) for the dividend, FB is a long party on 60 shares of stock X through the total return swap and a short party on the call option. Because the option has a delta of less than 0.8 at the calculation time, it is not a section 871(m) transaction. Therefore, there will be no dividend equivalent payments made by FB to the customer that are subject to withholding.

Under reg. section 1.1441-1(b)(4)(xxii), the broker is not obligated to withhold tax on the dividend equivalents on stock X paid to FB because the broker has valid documentation that it may rely upon to treat the dividend equivalents as paid to FB acting as a QDD.

The net delta exposure is zero at the end of the day on the date provided in subparagraph (j)(2) for the dividend because:

FB has a long position of 60 shares because of the total return swap; minus

FB’s short position of 60 shares because of the option.

Example 3 illustrates an in-the-money call option contract (meaning the contract price is less than the spot price) entered into by a foreign equity derivatives dealer that is hedged by ownership of the underlying security. The facts are the same as Example 2, but the customer purchases from FB an in-the-money call option on 100 shares of stock X with a term of one year. The call option has a delta of 0.8, and FB hedges the call option by purchasing 80 shares of stock X, which are held in an account with the broker, who also acts as paying agent.

The price of stock X declines substantially and the option lapses unexercised. At the end of the day on the date provided in subparagraph (j)(2) for the dividend, the call option has a delta of 0.48 and FB has reduced its hedge to 50 shares of stock X with the broker. Also on that date, FB owns no other shares of stock X or any other transactions that reference stock X in its equity derivatives dealer capacity.

At the end of the day on the date provided in subparagraph (j)(2) for the dividend, FB is a long party on 50 shares of stock X and a short party on an option. Because the option has a delta of 0.8 at the calculation time, it is a section 871(m) transaction. Therefore, FB is required to withhold tax on dividend equivalent payments to the customer on the option contract in accordance with reg. section 1.1441-2(e)(7).

The broker is required to withhold tax on the dividends paid to FB. Assuming that FB is a qualified resident of a country with a treaty that allows withholding on dividends at a 15 percent rate, the broker is required to withhold tax on the dividends paid on the 50 shares of stock X held by FB.

FB’s net delta exposure is two shares of stock X at the end of the day on the date provided in subparagraph (j)(2) because:

FB has a long position of 50 shares; minus

FB’s short position of 48 shares because of the option.

FB’s section 871(m) amount is $0.50 ($0.50 = net delta exposure of two shares * $0.25 dividend per share). FB’s section 881 tax on the $0.50 is reduced (but not below zero) by the section 881 tax paid by the QDD.

Notice 2022-37 extends transition relief provided in Notice 2020-2, 2020-3 IRB 327, for two years through 2024. The notice provides a useful summary of the history of regs under section 871(m) and successive extensions of their applicability dates.

General Extensions

Published June 14, 2010, Notice 2010-46, 2010-24 IRB 757, addresses potential overwithholding on securities lending and sale-repurchase agreements. It provides a two-part solution to the problem of overwithholding on a chain of dividends and dividend equivalents.

First, it provides an exception from withholding for payments to a qualified securities lender (QSL). Second, it provides a proposed framework to credit forward prior withholding on a chain of substitute dividends paid on a chain of securities lending, or stock repurchase agreements.

The QSL regime requires the person that agrees to act as a QSL to comply with withholding and documentation requirements. Treasury and the IRS permitted withholding agents to rely on transition rules provided in Part III of Notice 2010-46 until guidance was developed that would include documentation and substantiation of withholding.

The preamble to the 2015 temporary regs (published with the 2015 final regs and finalized in 2017) indicated that final QDD regs would supplant the framework proposed in Notice 2010-46. Published July 18, 2016, Notice 2016-42, 2016-29 IRB 67, contained a proposed QI agreement that included provisions relating to the QDD regime and reiterated the intent to replace the framework proposed in Notice 2010-46 with the QDD regime.

Published December 19, 2016, Notice 2016-76, 2016-51 IRB 1, provided for the phased-in application of some provisions of the section 871(m) regs to allow for their orderly implementation and announced that taxpayers may continue to rely on Notice 2010-46 until January 1, 2018. The applicability dates in the 2017 final regs reflect the phased-in application described in Notice 2016-76 (see reg. section 1.871-15(r)).

Published January 17, 2017, Rev. Proc. 2017-15, 2017-3 IRB 437, sets forth the final QI agreement (2017 QI agreement), including the requirements and obligations applicable to QDDs, and provided that taxpayers may continue to rely on Notice 2010-46 during 2017.

Consistent with Notice 2016-76, the 2017 final regs’ preamble made Notice 2010-46 obsolete as of January 1, 2018. In response to a comment requesting that the QSL regime remain, the preamble noted that while the QSL regime was administratively more convenient for taxpayers than the QI regime, it created administrability problems for the IRS, especially verification. The QSL regime was replaced by incorporating the QDD rules into the existing QI framework, including rules for pooled reporting on Form 1042-S and the QI requirements for compliance review and certification.

Published August 21, 2017, Notice 2017-42, 2017-34 IRB 212, extended some of 2016 transition relief. Published February 5, 2018, Notice 2018-5, 2018-6 IRB 341, permits withholding agents to apply the transition rules from Notice 2010-46 in 2018 and 2019.

Published October 1, 2018, Notice 2018-72, 2018-40 IRB 522, further extended transition relief and permitted withholding agents to apply the transition rules from Notice 2010-46 in 2020. Published January 13, 2020, Notice 2020-2, extended the phase-in period described in Notice 2018-72 through 2022. This most recent Notice 2022-37 further extends that phase-in period through 2024.

QDD Extension

Part V of Notice 2022-37 is dedicated to describing the extension of phase-in relief for QDDs. In 2015 reg. section 1.871-15T(q)(1) provided that when a QDD received a dividend or dividend equivalent payment and was obligated to make an offsetting dividend equivalent payment on the same underlying security in an amount that was less than the amount received, the QDD would be liable for tax under section 871(a) or 881 for the difference.

Reg. section 1.1441-1(b)(4)(xxii) of the 2015 final regs provided that a withholding agent who made a payment of a dividend to a QI acting as a QDD was not required to withhold on that payment if the withholding agent reliably associated the payment with a valid QI withholding form containing a certification described in reg. section 1.1441-1(e)(3)(ii)(E). The 2017 final regs adopted the net delta exposure method.

In adopting the net delta exposure method, however, Treasury and the IRS were concerned that the exemption from withholding on dividends paid to a QDD combined with the net delta exposure method could cause U.S.-source dividends to escape U.S. tax completely. Therefore, the 2017 final regs revised reg. sections 1.871-15(q)(1) and 1.1441-1(b)(4)(xxii) to provide that a QDD remains liable for tax under section 881(a)(1) and subject to withholding under chapters 3 and 4 on dividends.

However, to allow taxpayers time to implement the net delta exposure method, the 2017 QI agreement and final regs provided that dividends and dividend equivalents received by a QDD in its equity derivatives dealer capacity in 2017 will not be subject to tax under section 881(a)(1) or withholding under chapters 3 and 4.

Notices 2017-42, 2018-72, and 2020-2 announced that Treasury and the IRS intend to amend reg. sections 1.871-15(q)(1) and (r)(3), and 1.1441-1(b)(4)(xxii)(C) to provide that a QDD will not be subject to tax on dividends and dividend equivalents received in 2017-2022 in its equity derivatives dealer capacity or withholding on those dividends (including deemed dividends).

This notice again announces that Treasury and the IRS intend to amend those provisions to provide that a QDD will not be subject to tax on dividends and dividend equivalents received in 2023 and 2024 in its equity derivatives dealer capacity or withholding on those dividends (including deemed dividends).

Section 4.01(1) of Rev. Proc. 2017-15 provides that a QDD will be required to compute its section 871(m) amount using the net delta exposure method beginning in 2018. Notices 2017-42, 2018-72, and 2020-2 provided that a QDD would be required to compute its section 871(m) amount using the net delta exposure method beginning in 2023. This notice provides that a QDD will be required to compute its section 871(m) amount using the net delta exposure method beginning in 2025.

A QDD will remain liable for tax under section 881(a)(1) on dividends and dividend equivalents that it receives in any capacity other than as an equity derivatives dealer and on any other U.S.-source fixed, determinable, annual, and periodic payments that it receives (whether or not in its equity derivatives dealer capacity). Also, a QDD is responsible for withholding on dividend equivalents it pays to a foreign person on a section 871(m) transaction, whether acting in its capacity as an equity derivatives dealer or otherwise.

Finally, section 10.01(C) of the 2017 QI agreement provides that, for calendar year 2017, a QDD is not required to perform a periodic review of its QDD activities (as required by section 10.04 of the agreement) or provide the factual information specified in Appendix I. Notices 2017-42, 2018-72, and 2020-2 provide that a QDD is not required to perform a periodic review of its QDD activities for 2017-2022.

This notice provides that a QDD is not required to perform a periodic review of its QDD activities for 2023 or 2024. Treasury and the IRS anticipate including in the 2023 QI agreement the waiver of a QDD’s periodic review and the other transitional provisions for QDDs for 2023 and 2024.

QSL Extension

Notices 2018-5, 2018-72, and 2020-2 provide that, notwithstanding the 2017 regs’ preamble rendering Notice 2010-26 obsolete, withholding agents may apply the QSL transition rules in Notice 2010-46 for payments made in 2018-2022. This notice provides that withholding agents may also apply those QSL transition rules for payments made in 2023 and 2024.

Mon, 21 Aug 2023 00:08:00 -0500Carrie Brandon Elliottentext/htmlhttps://www.forbes.com/sites/taxnotes/2023/08/21/tax-regs-address-overwithholding-with-qualified-derivatives-dealers-exemption/Killexams : EHang Reports Second Quarter 2023 Unaudited Financial Results

- All Planned Tests for EH216-S Type Certification Completed 100%

- Strategic UAM Operational Partnership with Shenzhen Bao’an District

- US$23 Million Strategic PIPE Investment to Strengthen Liquidity

GUANGZHOU, China, Aug. 17, 2023 (GLOBE NEWSWIRE) -- EHang Holdings Limited (“EHang” or the “Company”) (Nasdaq: EH), the world’s leading autonomous aerial vehicle (“AAV”) technology platform company, today announced its unaudited financial results for the second quarter ended June 30, 2023.

Financial and Operational Highlights for the Second Quarter 2023

Total revenues were RMB10.0 million (US$1.4 million), compared with RMB22.2 million in the first quarter of 2023, as some deliveries have been extended to be post type certification (“TC”) of EH216-S per customers’ requests in light that the TC process is approaching the end.

Gross margin was 60.2%, representing a continued high gross margin level with a slight decrease of 3.7 percentage points compared to 63.9% in the first quarter of 2023, mainly due to the changes in revenue mix.

Operating loss was RMB75.3 million (US$10.4 million), compared with RMB75.7 million in the first quarter of 2023.

Adjusted operating loss1(non-GAAP) was RMB51.3 million (US$7.1 million), compared with RMB34.3 million in the first quarter of 2023.

Net loss was RMB75.7 million (US$10.4 million), compared with RMB87.0 million in the first quarter of 2023.

Adjusted net loss2(non-GAAP) was RMB51.8 million (US$7.1 million), compared with RMB33.6 million in the first quarter of 2023.

Cash, cash equivalents and restricted short-term deposits balances were RMB160.7 million (US$22.2 million) as of June 30, 2023, and increased to RMB320.6 million (US$44.9 million) as of July 31, 2023 after the closing of the US$23 million strategic PIPE investment.

Sales and deliveries of EH216 series AAVs3 were 5 units, compared with 11 units in the first quarter of 2023.

Business Highlightsfor the Second Quarter 2023 and recent Developments

All Planned Tests for EH216-S Type Certification Completed 100%

The Company has achieved a significant milestone for EH216-S TC by successfully completing all of the planned tests and flights in the last phase of demonstration and verification of compliance, and also completed the definitive TC Flight Test by the Civil Aviation Administration of China (“CAAC”), with unwavering endeavors throughout past 31 months since the CAAC officially accepted the Company’s TC application in January 2021. After finishing the remaining procedures, the Company expects to obtain the type certificate of EH216-S Unmanned Aerial Vehicle (“UAV”) System from the CAAC soon.

Delivered 5 Units of EH216-S AAVs to Joint Venture withShenzhen-listed Xiyu Tourism

In the second quarter of 2023, EHang established a joint venture with Xiyu Tourism (300859.SZ), a Shenzhen-listed leading tourism company in China and delivered 5 units of EH216-S AAVs to the joint venture. The customer aims to develop low-altitude tourism and sightseeing projects with EHang AAVs in the Heavenly Lake of Tianshan, a national 5A-class tourist attraction, and other scenic areas in Northwestern China. The partnership consists of plans to operate a minimum of 120 units of EH216-S or EHang’s comparable passenger-carrying AAVs within the next five years.

Strategic UAM Operational Partnership with Shenzhen Bao’an District

In July 2023, EHang reached a Memorandum of Understanding (“MOU”) with the Bao’an District Government of Shenzhen municipality on a strategic partnership for urban air mobility (“UAM”) operations after the certification of EH216-S. Both parties will jointly develop UAM use cases, systems, and routes to build Shenzhen as a national low-altitude economy development demonstration city. EHang plans to establish a UAM Operation Demonstration Center at the OH Bay in Shenzhen and launch aerial tourism and sightseeing experience services with EH216-S AAVs.

Continued Trial Operations of EH216-S in China

Under the CAAC’s guidance and the Company’s 100 Air Mobility Route Initiative, EHang, along with its customers and partners, have developed a total of 20 trial operation sites across 18 cities in China during the two years prior to the end of July 2023. More than 9,300 safety-ensured operational trial flights for low-altitude tourism and aerial sightseeing have been conducted by EH216-S at these sites, which paves the way for future commercial operations following the certification.

Extended Flight Footprints in Asia and Europe